Who's eligible?

What if my child was born prior to January 1, 2025, but is under age 18?

When and how can I open a Trump Account?

Once created, where can I find the account?

Who can conribute to a Trump Account and how much?

Are contributions to Trump Accounts tax deductible?

What are the funds invested in?

When can my child withdraw the money?

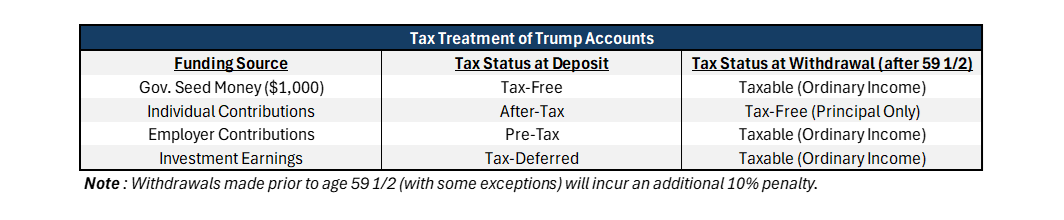

How are withdrawals taxed?