Kevin Dick

Posted on Jun. 4, 2026

In our previous article, we explored the “true” cost of homeownership by breaking down the four core components of a mortgage payment: principal, interest, taxes, and insurance (PITI). From there, we examined the financial impact of each element to arrive at what we called the Net House Payment.

While the Net House Payment is a valuable starting point for comparing renting and buying, there are many other factors in play when making such a large investment decision. For example, every dollar committed to a mortgage means one less dollar that can be invested elsewhere. So, the question then becomes, “When does it mathematically make more sense to buy instead of rent?”

In this article, we’ll examine how to use the Net House Payment to identify the moment at which the equity built through homeownership surpasses the potential growth of investing your available cash as a renter. The goal isn’t to determine which option is “better,” but rather to understand how long it may take for buying to become the financially advantageous choice.

The Homeowner’s Equity Engine

As discussed in part one, only one component of your mortgage payment actually builds your net worth: principal. Unlike interest, taxes, or insurance, principal isn’t an expense. Instead, it should be viewed as an investment.

Two key tailwinds work in the homeowner’s favor over time. The first is amortization. In the early years of a mortgage, the majority of each payment goes toward interest with only a small portion reducing the loan balance. As time goes on, however, that balance flips. More of each payment goes toward principal than interest, meaning the rate at which the homeowner is able to build equity slowly increases month after month.

The second tailwind is home value appreciation, assumed to equal 3% per year [1]. While the homeowner is building equity the traditional way by paying down mortgage principal, they’re simultaneously building equity passively as the home rises in market value. This is particularly attractive because it’s a function of the home’s full market value — not just the homeowner’s equity stake in it. For example, after just one year, a 3% increase on a $750,000 home generates $22,500 in added equity, despite the homeowner only having put $100,000 down. That’s the leverage of homeownership working in the background.

[1] “What is the average home value increase per year?” Credit Karma.

The Renter’s Alternative: Investing the Difference

This breakeven exercise assumes that in both scenarios — renting and buying — you have the same monthly cash flow available, equal to the homeowner’s mortgage payment. In other words, even if your monthly rent is substantially lower than the monthly Net House Payment, the assumption is that the renter will invest the difference. For example:

Option 1 (Buy):

- Monthly mortgage = $4,960 (PITI)

- Net House Payment = $4,007

Option 2 (Rent and Invest):

- Monthly rent = $3,250

- Monthly investment = $757

($4,007 – $3,250 = $757)

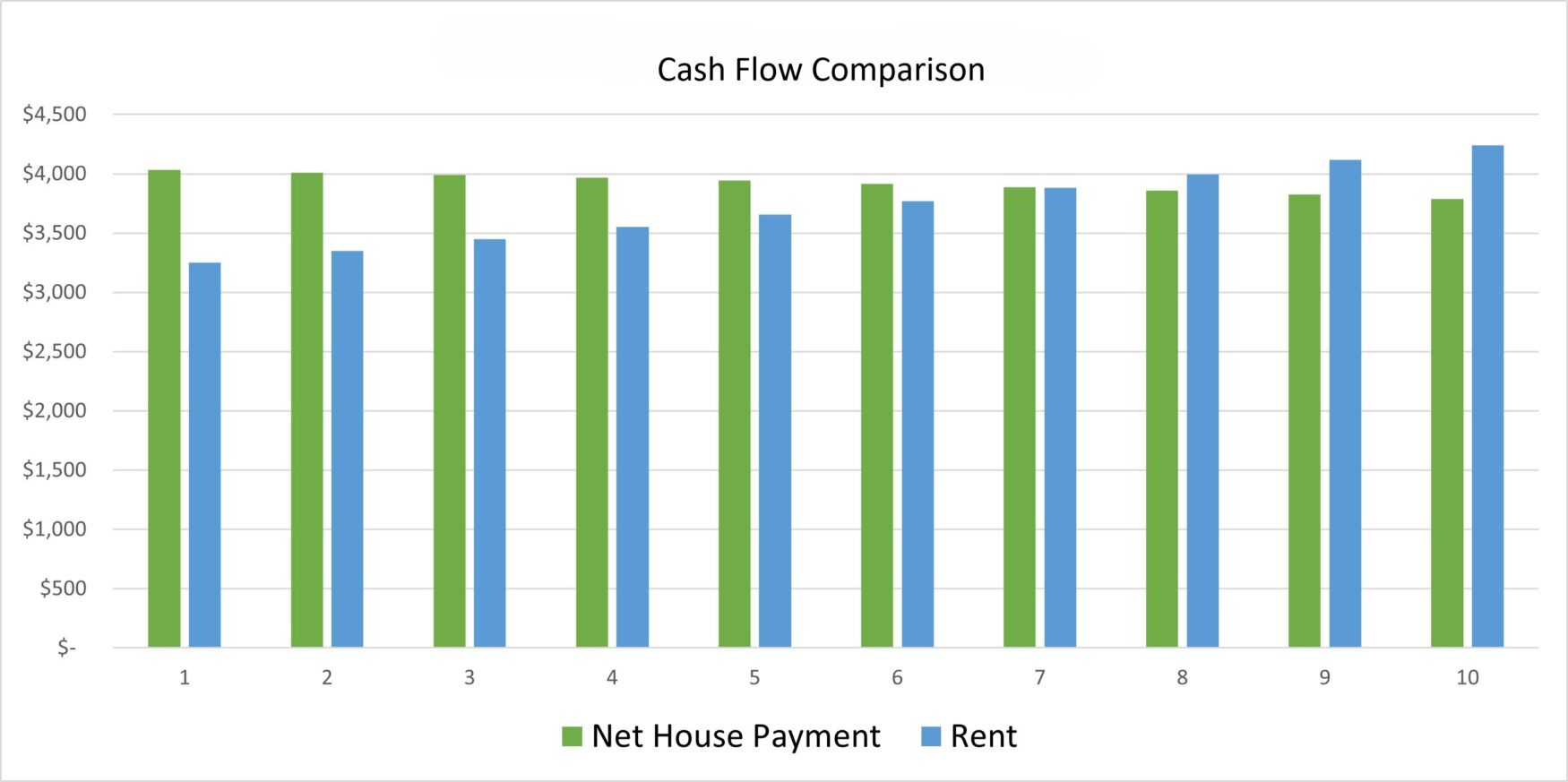

Let’s assume the renter earns a 7% annual return on their investments. Even though the $3,250 monthly rent payment goes completely out the door as an expense, the renter is able to dollar-cost-average the difference of $757 into the market each month. Even better, the renter keeps their down payment fully invested from day one, earning market returns on a lump sum that the homeowner now has tied up in a property appreciating at a more modest 3%.

However, the renter faces a significant headwind: inflation. Rent doesn’t stay at $3,250 forever. Assuming rent rises 3% annually, monthly rent becomes equal to the homeowner’s Net House Payment by year seven. At this point, the renter’s monthly surplus disappears entirely, and with it, their ability to keep investing the difference. By year ten, the math has completely flipped: owning the home is roughly $450 per month cheaper than renting.

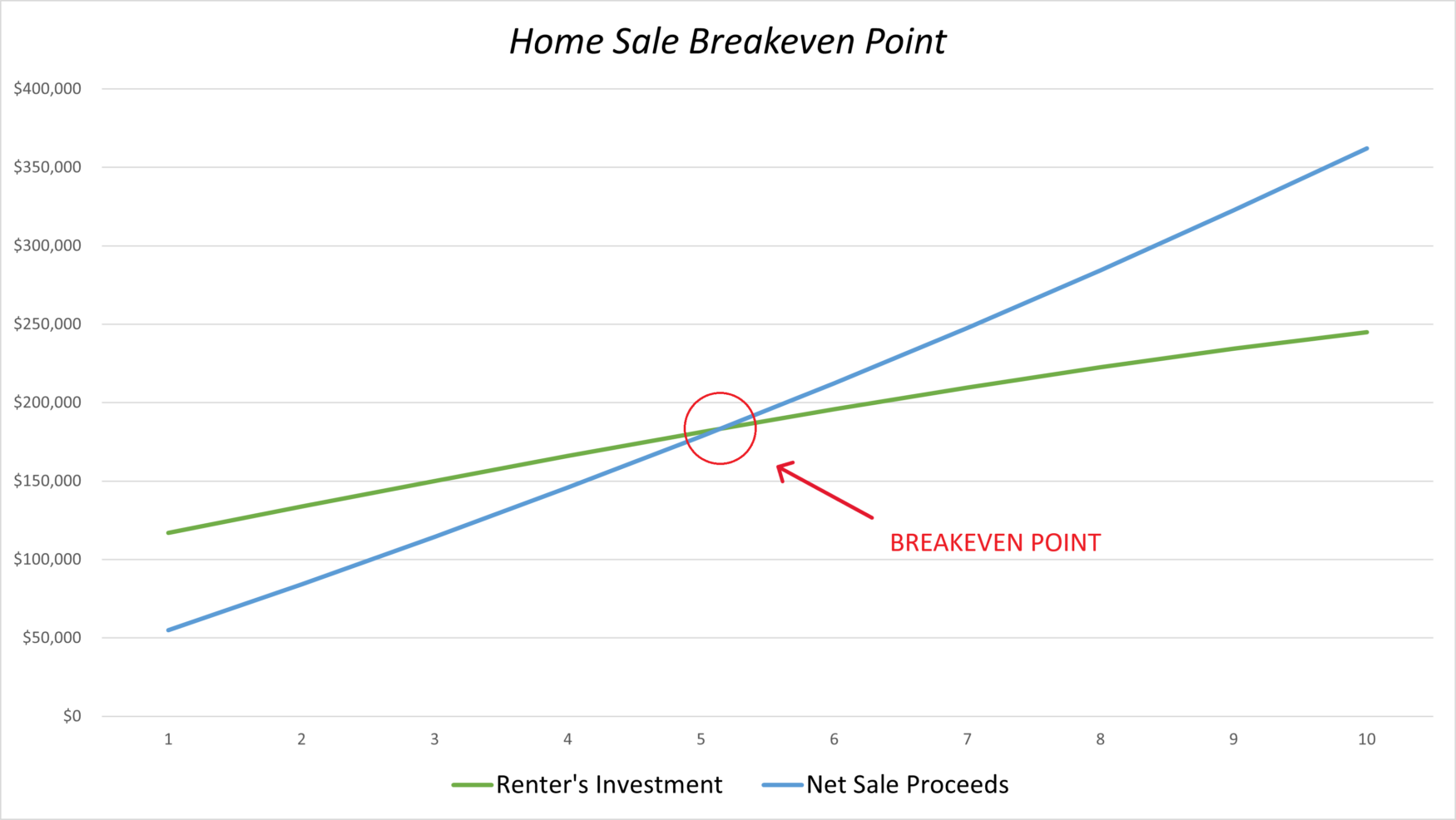

Breaking Even

Over time, the renter’s advantage is slowly being eroded by inflation in the form of rising rent. Meanwhile, amortization and home value appreciation are steadily increasing the pace at which the homeowner builds equity. The breakeven point is where those two curves intersect.

Refer to our example from part one:

- Home Price = $750,000

- Down Payment = $100,000

- Interest Rate = 6.00%

- Loan Term = 30 years

- Property Tax = 1.00%

- Annual Insurance = $2,000

- Private Mortgage Insurance (PMI) = 0.50%

- Income Tax Rate = 24%

The Net House Payment comes out to $4,007 in year one, against a monthly rent of $3,250 and an investable surplus of $757. After also accounting for the transaction costs of eventually selling the home (such as broker commissions), the breakeven point arrives at approximately five years. This means that, in this scenario, if you cannot commit to staying in the home for at least five years, then continuing to rent is likely the sounder financial decision. If you can, buying makes more sense.

Other Considerations

Like any financial model, this analysis rests on a set of assumptions. It’s worth being clear about where those assumptions may not hold.

The most significant limitation is behavioral. The renter’s entire value proposition depends on consistently investing the monthly surplus rather than spending it. In practice, lifestyle creep, unexpected expenses, and simple inertia can undermine even the best-laid plans. A mortgage, by contrast, functions as a form of forced savings. The equity gets built regardless of the homeowner being disciplined.

Also, it’s important to remember that markets don’t always go up and to the right. The 3% annual home value appreciation reflects historical averages, but real estate markets are cyclical (remember the 2008 housing crisis). The same can be said for the capital markets and your investment portfolio. So, the same leverage that passively builds your equity or portfolio returns can also work the other way.

Finally, it’s worth acknowledging the non-financial dimensions of the decision to buy a home. Stability, freedom, school districts, and proximity to family are just a few of the real-life factors that a spreadsheet can’t quantify. So is the flexibility that renting provides, such as the ability to relocate quickly for a job, relationship, or a change of scenery.

The breakeven point is a useful benchmark, but a decision this big deserves a more complete conversation. Meeting with your financial advisor is always the best place to start.

This content is provided for informational purposes only and should not be relied upon in any manner as professional advice, or an endorsement of any practices, products or services. There can be no guarantees or assurances that the views expressed here will be applicable for any particular facts or circumstances, and should not be relied upon in any manner. You should consult your own advisers as to legal, business, tax, and other related matters concerning any investment.