Tim Dick, CFP®

Posted on Mar. 26, 2026

Stock-based compensation is an extremely powerful way to build long-term wealth. Most, if not all, executives at Fortune 500 companies can point to their incentive stock plans as a primary driver of their generational wealth. Even more compelling, regular employees at some companies have reaped these benefits as well. For example, after becoming the greatest beneficiary of the so-called “boom” in artificial intelligence, “roughly 80% of Nvidia employees are now millionaires.”[1]

Of course, not all equity compensation appreciates in value, and employees are just as likely to hold a losing asset.

When it comes to stock-based compensation, Restricted Stock Units (RSUs) are the most common form. Unlike a traditional cash bonus, RSUs give you a direct stake in your company’s future, turning your hard work into potential equity. As the company achieves its performance milestones and the stock price appreciates, the value of your compensation can grow alongside it.

[1] “Nvidia Is Producing ‘Unprecedented Wealth’ For Its Employees, Nearly 80% Are Already Millionaires: Report,” Yahoo Finance.

RSU Basics

Navigating your equity requires an understanding of these core mechanics:

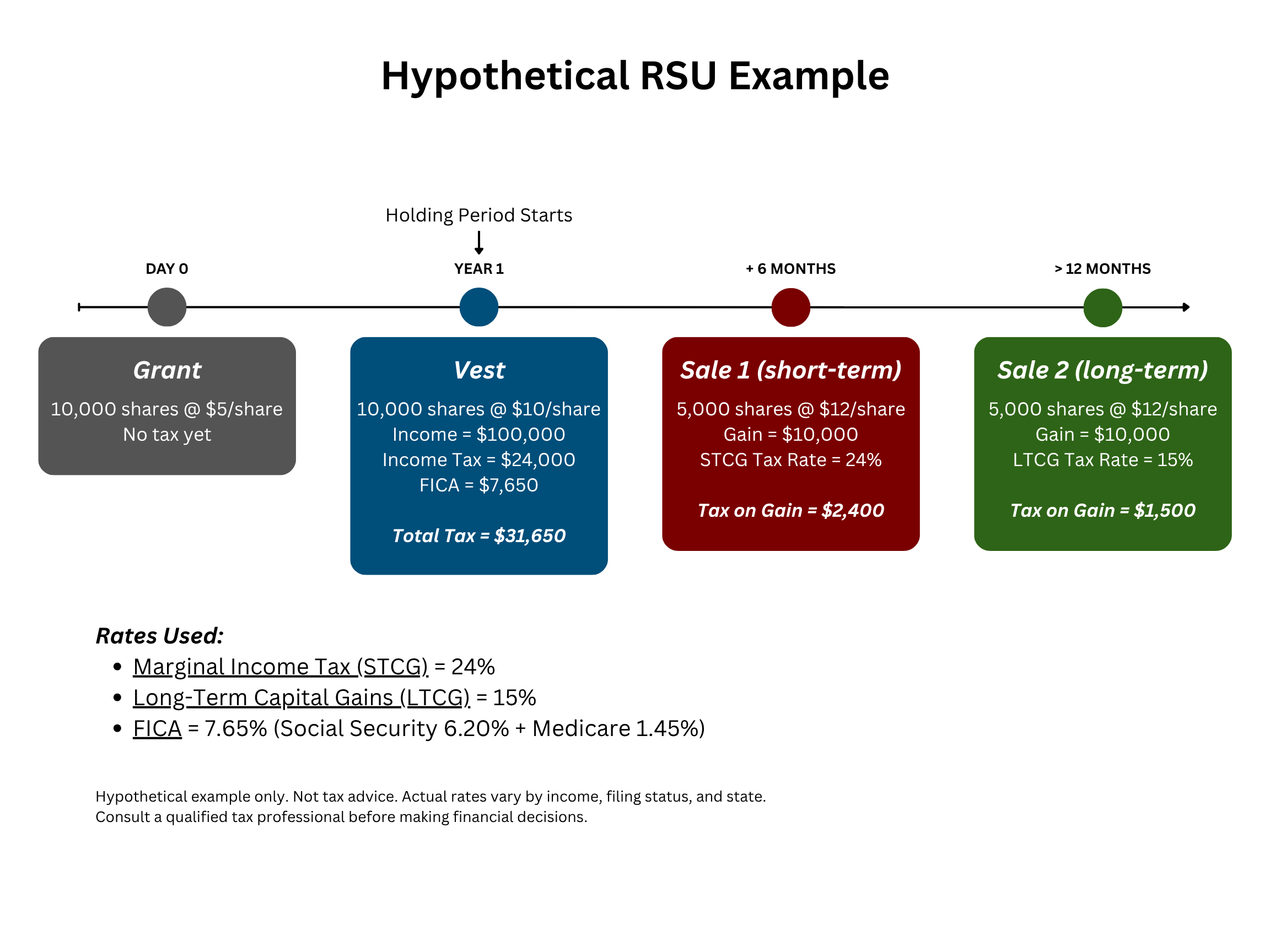

- Vesting – Your RSUs typically vest over several years (e.g., 25% per year). Notably, you do not own the shares, and they have no tangible value until each vesting date passes. Your holding period begins on the date of vest.

- Taxation – On the vesting date, the full market value is treated as ordinary income and taxed at your marginal rate, including applicable FICA taxes. Most companies use a “sell-to-cover” method to satisfy supplemental wage withholding, typically withholding a flat 22% on amounts under $1 million. If you’re in a higher tax bracket, this withholding may not fully cover your total tax liability.

- Liquidation – Once vested, you generally have the right to sell the shares for cash, provided you are not in a corporate “blackout period,” which typically happen around quarterly earnings reports.

Common Risk Factors

Without a well-designed strategy, RSU holders often face significant financial blind spots. A few things to consider when managing your RSU exposure:

- Phantom Tax Bill – If you do not withhold enough taxes at vest or fail to sell shares to cover the bill, you could face a sizeable tax liability with no liquidity to pay it, forcing you to liquidate other personal assets. Planning for the tax bill is essential when it comes to RSUs.

- Behavioral Hazards – Often times, people develop an emotional attachment to their company stock that can lead to investment mistakes. A plan removes the emotion of deciding whether to sell. It balances the risk of “selling too soon” against the danger of “holding too long” and watching wealth evaporate during a market downturn.

- Concentration Risk – It’s easy to end up with a portfolio dominated by a single stock. When your salary, health benefits, and future retirement savings are all tied to the same company, a corporate downturn can jeopardize your entire financial foundation simultaneously. You could find yourself laid off and with a depressed net worth.

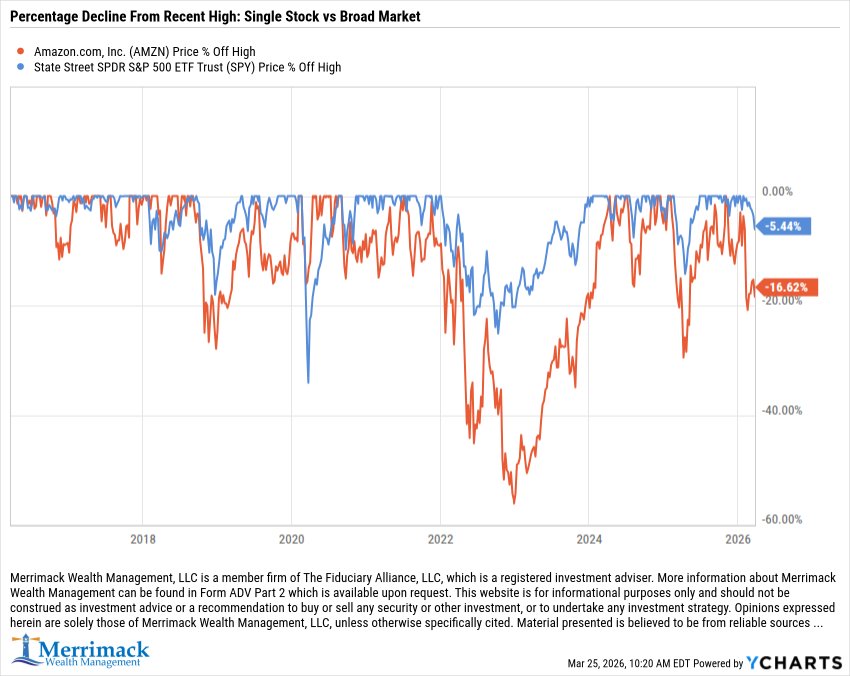

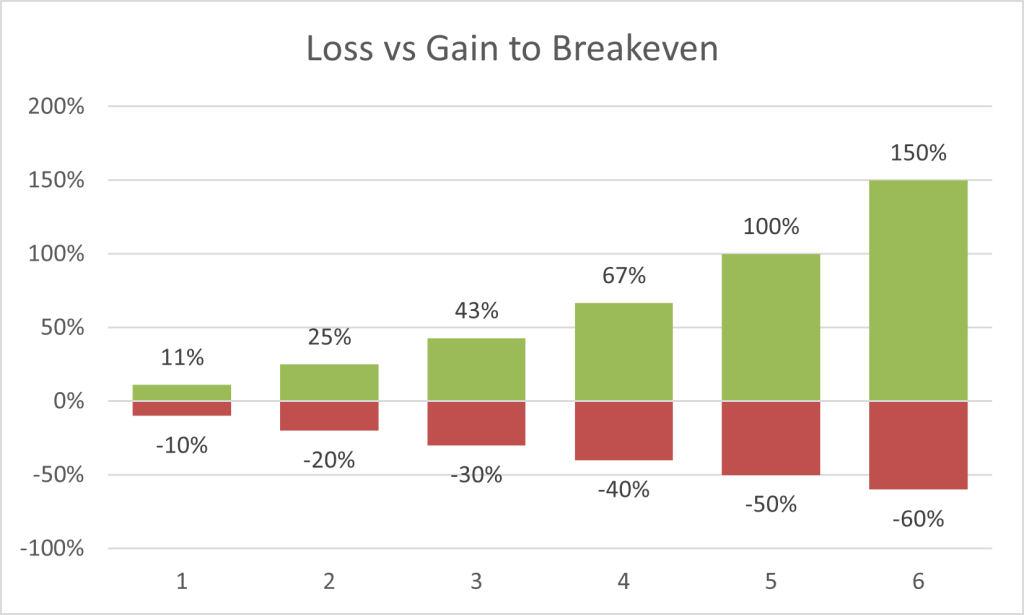

- Single Stock Volatility – Individual stocks are inherently more volatile than a diversified index; while a 30% to 50% drop is rare for a broad market, it is common for individual companies. Mathematically, a significant drop requires a much larger return just to break even. For example, a 50% loss requires a 100% gain to recover, and in some cases, a single stock price may never fully return to its original value.

Strategic Planning Considerations

To optimize your equity, we recommend looking at several advanced coordination strategies:

-

- Systematic Liquidation – Create a disciplined liquidation schedule that removes the emotion from your decision-making. Reinvest the proceeds in a diversified portfolio to reduce risk and/or set money aside for taxes.

- 10b5-1 Plans – For those with access to sensitive company information, these pre-scheduled trading plans allow you to sell stock legally during blackout periods, ensuring you stay on track with your diversification goals without regulatory mistakes.

- Tax Loss Harvesting – If some vested shares are trading below their original vesting price, selling those specific lots can generate a capital loss to offset capital gains elsewhere in your portfolio.

- Strategic Tax Deductions – In years with large RSU vests or stock sales, consider increasing retirement contributions or “bunching” charitable donations into a Donor-Advised Fund (DAF) to offset your higher taxable income.

This content is provided for informational purposes only and should not be relied upon in any manner as professional advice, or an endorsement of any practices, products or services. There can be no guarantees or assurances that the views expressed here will be applicable for any particular facts or circumstances, and should not be relied upon in any manner. You should consult your own advisers as to legal, business, tax, and other related matters concerning any investment.