Tim Dick, CFP®

Posted on Feb. 10, 2026

Philanthropy is one of the most virtuous endeavors one can undertake. While government programs provide a broad safety net, private charitable giving is often more nimble, capable of funding medical breakthroughs, supporting underprivileged groups, or responding to disasters in real-time. From a societal standpoint, charitable contributions provide the fuel for innovation and community care that might otherwise go unaddressed.

However, a truly impactful giving strategy is mutually beneficial. In other words, while your generosity supports recipient communities, the tax code incentivizes charitable giving by making donations tax deductible.

Donor Advised Funds (DAFs) were designed to democratize charitable giving to different causes around the country. DAFs have a surprisingly long history, but recent tax legislation has caused their popularity to surge among tax professionals and financial planners alike. By using a DAF, you can ensure your charitable heart works in perfect tandem with your financial brain.

Below-the-Line Deductions

Before exploring how charitable contributions to DAFs can lower your tax bill, it is important to understand the concept of “below-the-line” deductions.

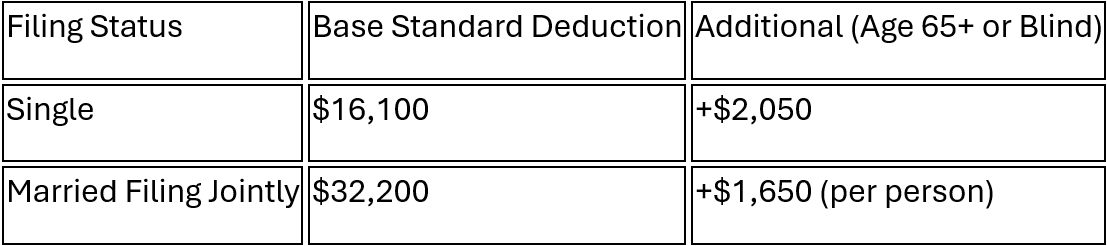

Every year, when you file your Form 1040, you have two primary options for lowering your taxable income. You can either claim the Standard Deduction or choose to Itemize Deductions.

1. Standard Deduction

The standard deduction is a flat amount available to all taxpayers. Following the Tax Cuts and Jobs Act (TCJA) of 2017, which significantly increased the standard deduction, and the “One Big Beautiful Bill Act” (OBBBA), which made these higher amounts permanent, the majority of Americans now choose this option.

The amount you can claim depends on your filing status and increases if you are at least age 65 or legally blind. For the 2026 tax year, the amounts are as follows:

Note: If you are a single filer who is both age 65 and blind, your total deduction would be $20,200 ($16,100 + $2,050 + $2,050).

2. Itemized Deductions

If your combined qualified expenses for the year exceed the standard deduction amounts listed above, it is in your financial interest to itemize. By listing these individual “below-the-line” expenses on Schedule A, you can reduce your taxable income even further.

Itemized expenses include:

- Charitable Contributions: Gifts to qualified non-profits (subject to certain AGI limits).

- State and Local Taxes (SALT): A combination of state income (or sales) tax and property taxes, currently capped at a total of $40,000 for 2026.

- Mortgage Interest: Interest paid on up to $750,000 of mortgage debt.

- Medical Expenses: Unreimbursed costs that exceed 7.5% of your Adjusted Gross Income (AGI).

- Casualty and Theft Losses: Losses incurred specifically in federally (or some state) declared disaster areas.

- Gambling Losses: Deductible only up to the amount of your gambling winnings.

Ultimately, taxpayers decide whether to use the standard deduction or itemize in a given year by utilizing the bigger of the two values. Most people take the standard deduction because it’s simple and often higher. However, for those with high mortgage interest, live in high state taxes, or have significant charitable donations, itemizing can be the key to unlocking substantial tax savings.

Strategic Planning

Over the course of someone’s financial plan, there will be years where we inevitably experience large spikes in total income, whether it’s selling a property, receiving a substantial bonus, exiting a business, etc. As planners, it’s in these years where we look to pull on the different levers at our disposal like itemizing deductions to rein in the tax burden.

Donor Advised Funds (DAFs)

A DAF is a dedicated charitable account held at a financial custodian like Charles Schwab that allows you to separate the timing of your tax savings from the timing of your actual giving. While many charitably inclined individuals might give smaller amounts annually, such as $5,000, those contributions often fail to exceed the standard deduction threshold, resulting in no additional tax benefit. By using a “bunching” strategy, you can contribute multiple years of giving (e.g., $50,000) into a DAF during a single high-income year to unlock a significant immediate deduction when you need it most. Once the DAF is funded, these assets can be invested to grow tax-free and are removed from your taxable estate, providing you the flexibility to recommend grants to your favorite causes over your lifetime or pass the account down as a multi-generational family legacy.

Taking it a step further, if you hold a concentrated portfolio with significant unrealized gains in a taxable brokerage account, perhaps as an early investor in companies like Apple or Nvidia, a DAF can be an exceptionally powerful solution. By contributing appreciated stock instead of cash, you bypass the capital gains tax entirely, while still receiving an immediate income tax deduction for the full market value of the shares (up to 30% of your AGI). This allows the charity to sell the security at its full value, effectively “cleaning” the tax liability from the growth while simultaneously helping you rebalance your portfolio and reduce single-stock risk.

Taking the Next Steps

Ready to transform your charitable giving into a powerful financial strategy? Our team can help you evaluate your current portfolio and income projections to determine if a Donor-Advised Fund is the right “lever” to pull for your tax and estate plan. Reach out to us today for a consultation to ensure your generosity is as tax efficient as it is impactful.

This content is provided for informational purposes only and should not be relied upon in any manner as professional advice, or an endorsement of any practices, products or services. There can be no guarantees or assurances that the views expressed here will be applicable for any particular facts or circumstances, and should not be relied upon in any manner. You should consult your own advisers as to legal, business, tax, and other related matters concerning any investment.